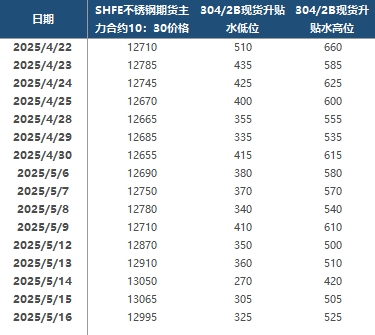

SMM reported on May 16 that stainless steel prices strengthened and rose overall this week. At the beginning of the week, positive news of a consensus reached in the US-China tariff negotiations rapidly boosted market confidence. Stainless steel futures prices took the lead in strengthening significantly, and the spot market soon followed suit. Driven by the market psychology of "rushing to buy amid continuous price rise and holding back amid price downturn," the previously suppressed pessimistic sentiment quickly dissipated. Market activity increased significantly, and transactions improved notably, driving a decline in social inventory of stainless steel. However, as time passed, by Friday this week, the effect of favourable macro front gradually weakened. After the downstream end-users' periodic procurement needs were met, market transactions turned weak again, and stainless steel prices also experienced a slight correction.

In the futures market, the most-traded contract 2507 weakened. At 10:30 a.m., SS2507 was quoted at 12,995 yuan/mt, down 70 yuan/mt from the previous trading day. In the Wuxi region, the spot premiums/discounts for 304/2B were in the range of 325-525 yuan/mt. In the spot market, the cold-rolled 201/2B coils in Wuxi and Foshan were both quoted at 8,050 yuan/mt. The average price of cold-rolled trimmed 304/2B coils was 13,275 yuan/mt in Wuxi and 13,225 yuan/mt in Foshan. The cold-rolled 316L/2B coils were priced at 23,870 yuan/mt in Wuxi and 23,875 yuan/mt in Foshan. The hot-rolled 316L/NO.1 coils were quoted at 23,100 yuan/mt in both regions. The cold-rolled 430/2B coils were both priced at 7,500 yuan/mt in Wuxi and Foshan.

Recently, multiple favourable macro factors, such as adjustments in US-China tariff policies and weaker-than-expected US CPI data, have combined to inject strong momentum into the stainless steel futures market, driving futures prices to continue climbing. The easing of tariff policies directly alleviated market concerns about export disruptions, while the weak US CPI data strengthened expectations for US Fed interest rate cuts, further boosting confidence in the commodity market. However, the market still faces numerous constraints: on the one hand, there is uncertainty about the final implementation effect and sustainability of the tariff policies; on the other hand, the supply of stainless steel continues to remain at historically high levels, and the supply-demand imbalance has not been fundamentally alleviated. Meanwhile, as the prices of raw materials such as high-grade NPI and high-carbon ferrochrome weaken, the cost side's support for prices has somewhat diminished. Against this backdrop, the actual recovery of end-use consumption in the downstream will become a key variable determining the trend of stainless steel prices, requiring continuous close attention.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)